Achievements from Trial Period 3

Note: This article refers to TP3, which ran from November 2022 to February 2023. The full report from the TP3 findings is available here. In this piece, we look at summarising what happened in TP3 and our main achievements and learnings for the future.

What did we do in TP3?

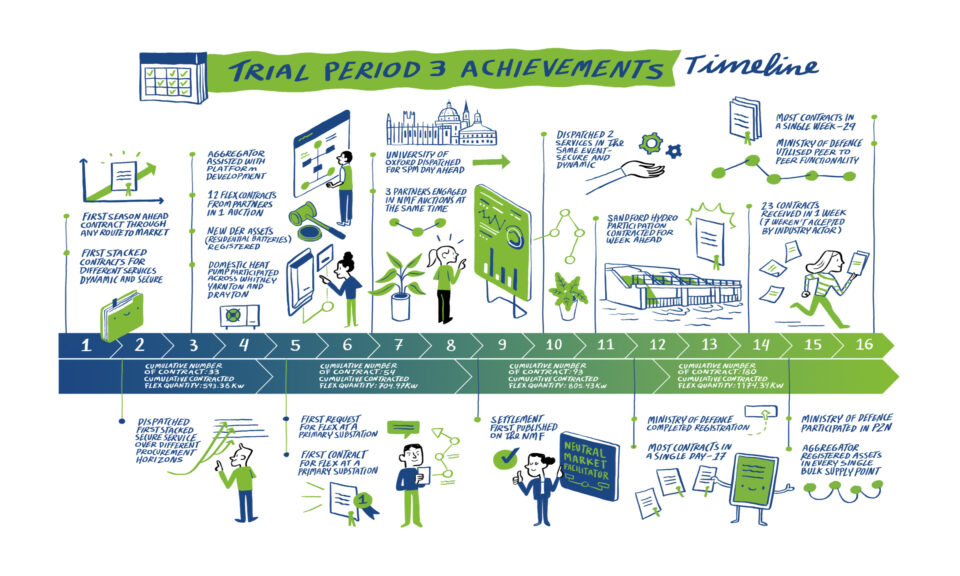

TP3 was a cumulation of the work TRANSITION carried out throughout Project LEO and during this time, we continued to build the complexity, scale, volume and number of events within the trials.

We delivered an increased number of auctions for energy flexibility, tested how different notice periods for providing this flexibility worked in improving participation in the auctions, and for the first time, we ran these at a more localised level, giving us valuable insight into how energy flexibility can be traded within communities behind their primary substations. We also developed a more complex market plan, where market participants can stack the services offered to maximise profitability.

To explain what this means:

An auction is an event where it is known that flexibility services will be needed to relieve pressure on the grid, for example, planned maintenance or peak usage times when excess energy use puts strain on the delivery and increase risks of outages.

The notice periods refer to the length of time given before the flexibility service is required, e.g. 1 week ahead or 1 day ahead and some services even operate with season ahead notice. We wanted to test how changing the notice period reflected on the number of participants in the auctions and the resulting contracts.

In terms of participants, we define these as organisations or households that interact with the market through a variety of DERs (generation or storage assets) that can offer energy flexibility. Examples of these are solar arrays, heat pumps, battery storage and hydro generation – some of these are domestic but many are commercial. Maximising the trading of flexibility from all of these assets requires the development of automation and a way of centrally monitoring each and this development formed a key part of our trials.

To give you an example of what we mean by services, two of these are Dynamic Constraint Management (DCM) and Secure Constraint Management (SCM) Services. These happen when a DER is asked to provide a flexibility service – either increasing generation (or discharging a battery) or decreasing demand in order to address an issue that has or may cause an outage – these services help the network operator to manage demand while they address the problem. Depending on the type of service required, there are a variety of notice periods to provide the services. There are four of these services in total.

In TP3 we looked at many of the background processes, technologies and management systems that need to be put in place so these kinds of services can run as business as usual across our networks.

Outlining Key Accomplishments in TP3

While TP3 continued to build on the work of the preceding trial periods, there were four main accomplishments that we can report on specifically to TP3 – these were:

Aggregators –

We continued to find that non-traditional market participants generally don’t have the time or resources to understand flexibility services and markets.

In TP3, a new market participant came on board in an aggregator role. Equiwatt manages and automates the energy usage and generation of a large number of domestic premises. As Equiwatt was already a partner in Project LEO, they had sufficient information to participate in auctions and choose the appropriate service.

Equiwatt as a partner acted successfully as an aggregator to advertise the need for flexibility to a much wider audience and include residential flexibility services via their technology (an app) and this involvement contributed to an increase in the number of and involvement in auctions across all service types and gave us valuable insight into how domestic assets can be integrated into a flexible energy marketplace.

Stacking Services

As outlined above, flexibility providers can participate in a number of different services to supply flexibility to the network. In return, they are remunerated in line with the service provided.

For the first time, in TP3, participants were able to participate in 2 services at the same time. So, we updated the complexity of our market offering so that participating assets could provide flexibility to the Distribution System Operator and the Electricity System Operator during the same auction.

The benefit of this stacking option is that the flexibility providers (participants) can receive higher remuneration for the service they provide and this increases the appeal of participation. The benefit to the marketplace is that, with higher rewards, more participants will enter.

Introducing Primary Markets

Another first within TP3 was the introduction of auctions at the Primary Substation level. This was the first time we trialled having assets bid to provide flexibility at a primary level for a number of services.

This was made possible by an improved network model that had not been available in TP1 or 2, which enabled us to zoom into communities, providing flexibility at the grid edge.

This achievement for TP3 is an important step forward for flexibility markets as it demonstrates how flexibility services can be traded at a more local level, giving communities more power over their energy use and generation. The trial identified the benefits and constraints of running auctions at this level which are vital learnings for the future development of this offering.

Including MOD in trials

Another key achievement of TP3 was the successful onboarding of the Ministry of Defence as a trial participant. The MOD has the potential to be a major supplier of flexibility services, given the vast number of assets, fleets and buildings it owns around the UK.

A major success for the Project LEO and TRANSITION market trials was including the MOD Oxford base in our trials to see to what extent they can deliver flexibility and define what this could mean if rolled out to all MOD bases around the UK as well as identifying what the potential operational and technical challenges are.

During TP3 we developed a proof of concept – in theory, MOD bases could have the potential to deliver flexibility to the network by shifting the ways they are run and reducing their energy use on demand while looking at ways they can potentially generate and store energy to provide even more flexibility and how they could bid in markets and earn a return for this. We also looked at the potential for the MOD to trade energy capacity between their bases.

The successful roll-out of the inclusion of MOD bases in energy flexibility markets could have a huge impact on the future roll-out of flexibility services to large organisations such as this, accellerating our transition to a net-zero energy system.

Overall learnings from TP3 and trials as a whole

Building on learnings from TP1 and TP2, TP3 provided many valuable additional learnings to inform the future of business-as-usual services and for developing and running energy flexibility markets in Oxford and the UK as a whole.

TP3 focused on increasing the involvement of market participants. It did this by looking at a much wider and more complex mix of energy generation and storage assets and conducting trials that look at how the marketplace technology, services and products would work for potential participants in everyday situations, gathering feedback to inform future development.

As the trials have progressed, we have learned a lot about what works and what doesn’t and the challenges that will need to be overcome for us to roll out these services as part of business-as-usual energy trading, especially in the automation of many of these services.

The success of data gathering and learning in TP3 was down to numerous factors, the key ones being:

- TP3 saw a significant increase in the number of auctions (where participants are invited to bid to provide flexibility services at a particular time) over the period, allowing us to gain more realistic insights into the opportunities and barriers for these.

- We learned that the timings for auctions were a major factor in success and participation, so we trailed different scenarios e.g. week ahead and day-ahead auctions.

- The introduction of the running of auctions at primary substations gives us additional insight into how these services could succeed at a more localised level.

- The introduction of stacking services makes participation more attractive by introducing additional revenue sources.

The full learnings and outcomes from TP3 can be found in this report but in summary, we see these as:

Understanding what the barriers are for communities and customers to participate in the flexibility marketplace – TP3 provided greater insight into what needs to be improved to provide a smoother experience for participants. We analysed feedback that suggests the number, complexity and length of the contractual arrangements present a barrier to participation.

The trials showed that more flexible contracts that allow market participants to take part in individual auctions without needing to sign additional contracts were effective in allowing SSEN to acquire flexibility over shorter timescales and will be looked at as a service going forward.

The application of a ‘whole portfolio approach’ and seamless automation makes taking part in flexibility services more attractive to potential participants. The introduction of stacking and the potential for increased revenue was seen as a positive development for both participants and the energy network and this will be explored further and rolled out widely.

The trials also identified potential barriers to the stacking of different revenue streams and this delivers important insights to help us develop the service for the future.

Primary liquidity – Improving participants’ ability to trade and be paid for energy flexibility at a more local level is key to providing a successful and rewarding flexibility market, but a number of barriers were identified through TP3 that need to be addressed. The insights we gained support the development of the “menu” of flexibility products that can be developed going forward.

TP3 also identified the need for a simpler and more accurate baseline model that will help us improve forecasts for flexibility services.

What’s next?

The published report on TP3 gives us a flavour of the challenges that still need to be overcome in developing a successful and reliable local market for energy flexibility. Following TP3, the projects have undertaken a Technical Trial to gain further feedback and insights.

The learnings from TP3 and the Project LEO / TRANSITION trials as a whole will help to produce a successful energy flexibility marketplace that can be more fully automated, removing many of the barriers to participation.

Thanks to the learnings from the marketplace trials, we are now moving towards a more accessible and less complex marketplace for trading energy flexibility and we have started to identify how this is viable as a business-as-usual process.

At SSEN TRANSITION, we are excited to put all of these learnings into action and further develop our systems and services to deliver the flexible and robust energy system we all need for a net-zero future.